25 Jan Should I convert my IRA to a Roth to qualify for N.J. benefits?

Photo: pixabay.comQ. I’m now almost 68, and based on my retirement savings in IRAs and 403(b) accounts, I think my Required Minimum Distributions (RMDs) will be almost $100,000 per year once they start. I intend to keep working part-time so my income will exceed this, plus I have Social Security. Eligibility for benefits like the Senior Freeze and pension exclusion, plus the cost of Medicare, would be affected by this. Does it make sense for me to convert a large amount to a Roth IRA now? In this year, I would lose eligibility for those benefits but then once the RMDs kick in, I would stay under the income threshold. Or is it crazy to incur a huge tax bill now?

— Planning ahead

A. Your question is a very good one and has many moving parts.

Before addressing your Roth IRA conversion question, let’s look at eligibility of the benefits available to New Jersey taxpayers if their income is below certain thresholds.

First, there is the New Jersey pension exclusion, under which certain taxpayers don’t have to pay taxes on retirement and pension income.

You qualify for the pension exclusion if you — and/or your spouse if you are filing jointly — are 62 or older or those who, because of a disability, are eligible for Social Security benefits, and you have $100,000 or less of gross income, said Gerard Papetti, a certified financial planner and certified public accountant with U.S. Financial Services in Fairfield.

He said for 2021, the exclusion for a married couple filing jointly is $100,000, it’s $50,000 for those married filing separately and it’s $75,000 for single filers.

Papetti said the income you must consider includes:

- Wages

- Taxable interest

- Dividends

- Net profits from business

- Net gains from the disposition of property

- Pensions, annuities, and IRA withdrawals

- Partnership income

- S-Corporation income

- Net income from rents, royalties, patents, copyrights

- Net gambling winnings

- Alimony

- Any other taxable income subject to New Jersey tax

Papetti said you do not have to include, for pension exclusion purposes:

- Social Security income you receive

- Pension income from private or public sector as a result of permanent or total disability received prior to age 65. Once the disabled taxpayer attains age 65 the pension income is no longer exempt and is included.

- U.S. Military or Survivor’s pension benefits

- Tax-Exempt interest from obligations of the State of New Jersey or any of its political subdivisions or interest from direct federal obligations, such as U.S. Savings Bonds and US Treasury Bills, Bonds, and Notes.

Then there’s the New Jersey Senior Freeze program.

“This reimburses eligible senior citizens and disabled persons for property tax or mobile home park site fee increases on their principal residence,” Papetti said. “To qualify, you must meet all the eligibility requirements for each year from the base year through the application year.”

The current application year is 2019.

To be eligible for the Senior Freeze, you or your spouse/civil union partners must be age 65 or older on Dec. 31, 2018, or receiving federal Social Security disability benefits on or before Dec. 31, 2018. You must have lived continuously in New Jersey since Dec. 31, 2008 or earlier as a homeowner or renter.

Your property taxes must be paid in full, and your total income, if married, must be $89,013 in 2018 and $91,505 in 2019.

“The Senior Freeze program reimburses homeowners for any property tax increases you have once you are in the program,” Papetti said. “Each year you are eligible you will receive the difference between your base year — the first year of eligibility — property tax amount and the current year property tax amount as long as the current year property tax is higher than the base year.”

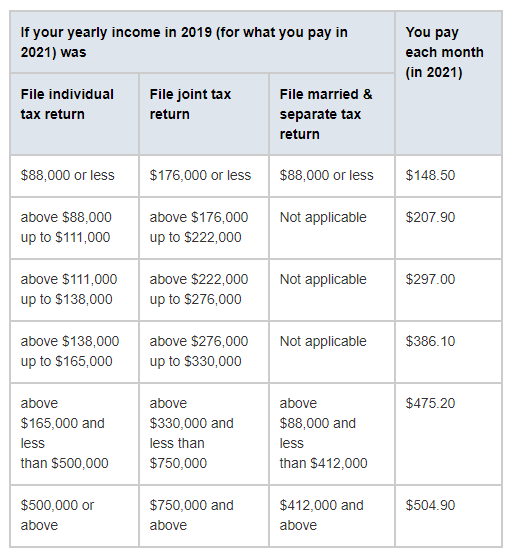

Then, as you mentioned, you could be subject to the Medicare Part B High Income Surcharge.

The standard Part B premium amount in 2021 is $148.50, Papetti said.

“But if your modified adjusted gross income (MAGI) as reported on your IRS tax return from two years ago is above a certain amount, you’ll pay the standard premium amount and an Income Related Monthly Adjustment Amount (IRMAA),” he said. “IRMAA is an extra charge added to your premium.”

The IRMAA, based on your 2019 MAGI, is as follows:

Source: Internal Revenue Service

Now to your question.

As you noted, converting from a traditional IRA to a Roth IRA will subject the conversion amount to income taxation.

“Typically timing and tax rates are crucial factors when making a decision, however the benefits you receive from the items noted above may provide more of a reason to convert that purely tax rates and timing,” Papetti said.

So you have several items to consider when making this decision.

First, your time frame.

“In general, the longer you have before you need the money, the more sense it makes to convert your IRA to a Roth IRA,” Papetti said. “Once you convert to a Roth, qualified withdrawals including your conversion amount will never be taxed.”

Leaving those assets untouched to grow tax-free for as long as possible allows you to maximize the benefit of the conversion, Papetti said.

Then you should consider your tax rate. Papetti said when you convert, you want to do it at the lowest possible tax rate.

“In your situation you should review your current marginal tax brackets and try to convert an amount that will not place you in the next highest marginal tax rate,” he said.

Next, you have to decide how you will pay for the conversion.

“If taxes on the conversion are paid from IRA money, less is left in the Roth to grow, eroding the benefit of the conversion,” Papetti said. “The best practice is to pay the taxes due on conversion from cash on hand or taxable investments.”

If tapping your current IRA assets to pay the taxes is your only option, converting might be unwise, he said.

Then there are the Required Minimum Distributions (RMDs).

As you noted you are required to withdraw money from traditional IRA accounts starting at age 72, but you are not required to take money out of a Roth, Papetti said. If you don’t need to tap into IRA funds to cover living expenses, a Roth IRA gives you the freedom to choose when or if you take withdrawals over your lifetime.

The conversion will also have an impact on your estate plan.

“Roth IRAs are a better asset to pass on to your heirs than traditional IRAs,” he said. “Where traditional IRAs create taxable income, heirs don’t have to pay taxes on Roth IRAs, and they have more flexibility in drawing down the account.”

You should also consider where you plan to live in retirement, Papetti said. If you planned to live in a state that doesn’t have an income tax, like in Florida, a conversion may not be something you’d have to worry about.

Finally, think about whether you need all of the IRA funds to meet your income needs through retirement because “losing capital when you are retired to pay taxes is not recommended,” he said.

Given all these moving parts, you should speak to a qualified tax professional who can calculate the exact benefits you would receive from converting all or a part of your IRA to a Roth IRA, and compare it to the projected accumulation of your IRA if you did not convert and you receive RMDs instead.

Email your questions to .

This story was originally published on Jan. 25, 2021.

NJMoneyHelp.com presents certain general financial planning principles and advice, but should never be viewed as a substitute for obtaining advice from a personal professional advisor who understands your unique individual circumstances.