30 Nov Using a Roth IRA to pay for college

Photo: clconroy/morguefile.comQ. I have a Roth IRA that I was planning to leave to my kids. But now my grandchildren are getting ready for college. Can I somehow use the Roth money for their college without any bad tax consequences?

— Grandpa

A. Roth IRAs offer many benefits. Access to your contributions without penalty is one of them.

“The perk to a Roth IRA is that contributions are made post-tax and that earnings on the account are tax-free and withdrawals are also not subject to tax,” said Dean Shah, a certified financial planner with Stonegate Wealth Management in Oakland.

There are a few rules, though.

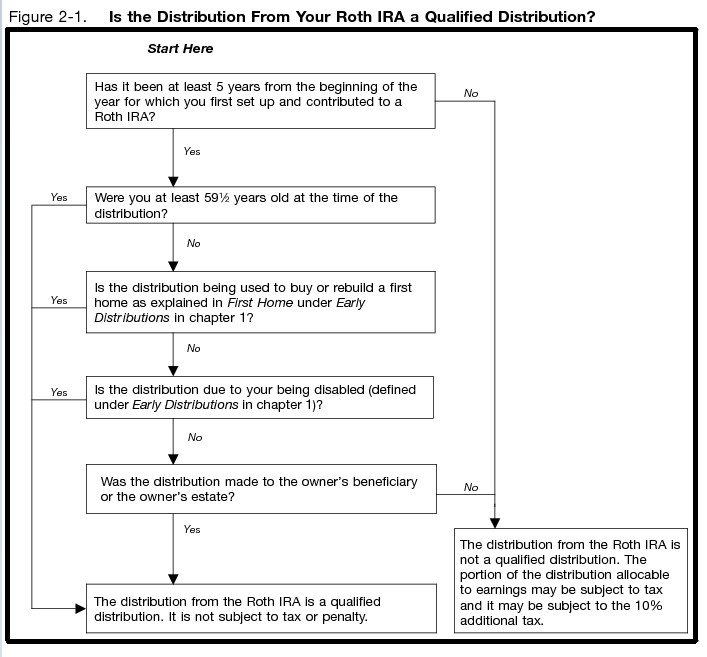

If you have had the Roth IRA open for at least five years and you are at least age 59½, you can make withdrawals with no penalty or tax ramifications, Shah said. If the account has been open for less than five years, your interest/gain will be taxable when you make the withdrawal.

For those who are younger than 59 1/2, you can also take out your contributions, but if you take out the earnings, they could be taxed and subject to the penalty.

Check out the figure below from IRS Publication 590-B.

Shah said the reason for the withdrawal doesn’t matter, so you can certainly use it to fund college,” he said.

Just make sure you won’t need the money for yourself.

You didn’t say how much you’re thinking of withdrawing or the cost of the college bills. You’ll have to be careful about gifting rules here.

But there’s a trick.

“If you pay the college directly, then the gift is not subject to the annual gift limit,” said Vince Pallitto, a certified financial planner and certified public accountant with Summit Asset Management in Florham Park.

And if you have extra cash and you want to give your grandchildren a head start for retirement, you can also open Roth IRAs for your grandchildren under certain circumstances.

Email your questions to Ask@NJMoneyHelp.com.

This story was first posted in December 2015.

NJMoneyHelp.com presents certain general financial planning principles and advice, but should never be viewed as a substitute for obtaining advice from a personal professional advisor who understands your unique individual circumstances.