08 Mar Retirement and Roth IRA conversions

Photo: nicksumm/morguefile.comQ. I’m going to retire next year, and I have a traditional IRA worth $260,000 that I’m thinking of converting to a Roth. I don’t think I will need the money during my retirement, so I love the idea of giving a tax-free gift to my kids. What should I consider?

— Almost there

A. Congratulations on your upcoming retirement.

While Roth IRAs offer tax advantages, converting from a traditional IRA to a Roth could present some problems.

First, realize you will have to pay tax on the amount you are converting because the government considers the amount converted to be income, said Timothy Brunnock, a financial advisor and attorney with Trinity Financial Strategies in Morristown.

“By converting it all at one time, you will have added $260,000 to your taxable income for that year,” Brunnock said. “This means that you will pay taxes on the full $260,000 — together with any income you earn from your job.

While we don’t know your age or the amount of your annual income, such a conversion would in all likelihood move you into a higher income tax bracket, Brunnock said.

One possibility is to make the conversion over multiple years, Brunnock.

“This will ease your tax burden over time, and may keep you in a lower tax bracket,” he said.

Michael Green, a certified financial planner with Wechter Feldman Wealth Management in Parsippany, said perhaps one of the most important factors in your decision is whether or not you can afford to fund the tax bill without hurting your retirement plan.

Green said if you choose to pay taxes from your IRA principal, converting may not provide the best long-term result.

“By paying income taxes from other out-of-pocket sources, you keep your IRA balance intact, thus allowing the converted Roth IRA to fully take advantage of tax-free growth over time,” he said.

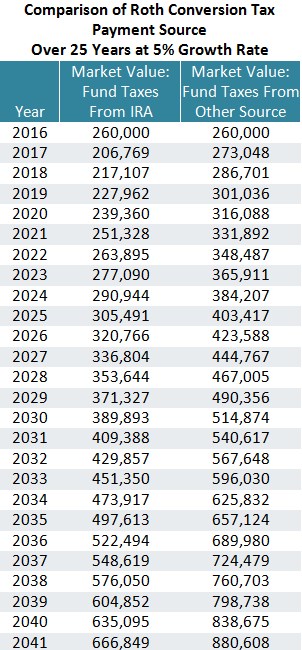

He offered this chart, which illustrates the difference between paying taxes from your IRA in comparison to other out-of-pocket sources.

Green said in this example, the taxes owed on the Roth conversion come to $66,280. He said the calculation is based on a married couple filing jointly with no additional taxable income in 2016.

“A full Roth conversion lands the couple in a 33 percent marginal tax bracket for federal income taxes and 6.37 percent marginal tax bracket for New Jersey,” Green said. “Since it’s likely you will have other sources of taxable income, you may be pushed into a higher bracket.”

Green said you should consider your anticipated income changes to determine when and how much of your IRA should be converted to help minimize taxes. You also have the option to spread the conversion over multiple years, potentially reducing your marginal tax rate and spreading your tax obligation, he said.

It appears your question is geared largely toward the effect of a Roth IRA conversion on estate planning, as you mention leaving a tax-free gift to your children.

“Although your Roth IRA would grow tax-free, the balance may be subject to estate tax at both federal and state levels,” Greens said.

The federal estate tax exemption for 2016 is $5.45 million per individual and could be double that for a married couple. That means as long as your estate is smaller than the exemption, you will not owe estate taxes to the federal government, Green said. For New Jersey, the estate tax exemption is only $675,000.

“After inheriting your Roth IRA, your kids would be required to take distributions over their lifetime, over a five-year period, or as a lump sum,” Green said. “Ideally, distributions will be taken over their lifetime since undistributed assets can continue to grow tax-free.”

On your comment about thinking you won’t need the money in retirement, Brunnock said he has some concerns.

“It is imperative to do a detailed retirement income analysis before gifting any money,” he said. “A good financial advisor can help you figure this out, based upon your guaranteed sources of income, anticipated returns on your other investments, estimated expenses in retirement and your estimated lifespan.”

Sounds like you should also meet with your tax preparer and an estate planning attorney before you make any decisions.

Email your questions to .

This story was first posted in March 2016.

NJMoneyHelp.com presents certain general financial planning principles and advice, but should never be viewed as a substitute for obtaining advice from a personal professional advisor who understands your unique individual circumstances.