05 Jan Social Security: The odds are in your favor

Photo: kakiksy/morguefile.comQ. Now that file and suspend isn’t an option, what other strategies can we use to make sure we get as much as possible out of Social Security?

— Almost retired

A. The elimination of the file and suspend strategy has significantly changed the Social Security landscape.

The file and suspend strategy was one that would help couples get more out of lifetime Social Security benefits.

Prior to the change, the spouse with the higher benefit was able to file for Social Security retirement benefits once reaching full retirement age and then immediately suspend those benefit, said Michael Green, a certified financial planner with Wechter Feldman Wealth Management in Parsippany.

“This would allow that spouse’s benefit to continue accruing the delayed benefit at about a 8 percent increase per year up to age 70,” Green said.

At the same time, it would allow the lower earning spouse to file for restricted spousal benefits at full retirement age, which would equal 50 percent of the higher earning spouse’s benefit, Green said. This would delay the filing of the lower earning spouse’s own benefit, which would also continue to accrue.

Green said there are various grandfathering provisions for those already collecting or close to collecting their Social Security benefits.

But without the option to file and suspend, other options will become more commonly explored, Green said. For example, should a married couple file at age 62 or wait until full retirement age? Should one spouse file early and the other wait until full retirement age to file? Should one spouse file at full retirement age while the other waits until age 70 to accrue a larger benefit?

“The determination of which strategy to utilize is often based on a break-even analysis,” he said. “That is, how many years will each spouse need to live in order to make up for the forfeited benefits caused by delaying filing?”

Even with the recent law changes, Social Security planning is still a critical component of any retiree’s financial plan, said Amanda Lott, a certified financial planner with RegentAtlantic in Morristown.

“Social Security remains a rare asset,” she said. “It lasts as long as you do, and it keeps up with inflation.”

One of the biggest risks a retiree faces is “longevity risk”: The chance of running out of money before running out of life.

Lott said for many retirees, as long as you don’t have a seriously impaired life expectancy, it continues to make sense to delay benefits as long as possible and maximize the monthly check you’ll receive for life — or potentially your spouse’s life if they are likely to collect a survivor benefit off of your record once you pass away.

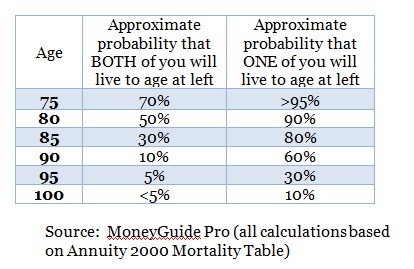

For a 65-year-old married couple, the longevity odds are in your favor.

As you can see in the chart, Lott said, there’s about a 30 percent chance that both individuals in a couple will live to age 85 and a 60 percent chance that at least one will make it to age 90.

“The `break-even age,’ which is the age to which an individual must live to make delaying benefits a better financial deal than collecting benefits as soon as possible, is typically the early 80s,” she said. “Depending on an individual’s or couple’s specific circumstances paired with the probabilities above, there’s a significant chance you would receive a higher cumulative value over your lifetime if you implement a Social Security strategy that incorporates some element of delaying benefits.”

Lott said it’s important to know that this advantage still holds true even if you are impacted by the recent law changes.

These potential additional dollars in your pocket are quite meaningful when you consider the importance of hedging against longevity risk, she said.

“Yes, there’s only a 10 percent chance that both members of a married couple will live to age 90,” Lott said. “However, I would argue that the risk of dying earlier and not having as much to pass on to beneficiaries is a much smaller risk than making it to your late 80s or beyond and not having money to pay the bills.”

She offers this comparison: The risk of your home burning to the ground is definitely not more than 50 percent, but you still insure the risk by buying home insurance. While the odds of making it past the Social Security break-even age are not more than 50 percent, there’s still a significant chance you could live beyond that point. Your Social Security benefit is a crucial tool to help mitigate that risk, and securing a higher benefit now can add to your financial security during your later years.

For many individuals, the new law will decrease the total Social Security benefits they’ll collect over their lifetimes, Lott said. However, there is still good reason to choose an effective Social Security strategy.

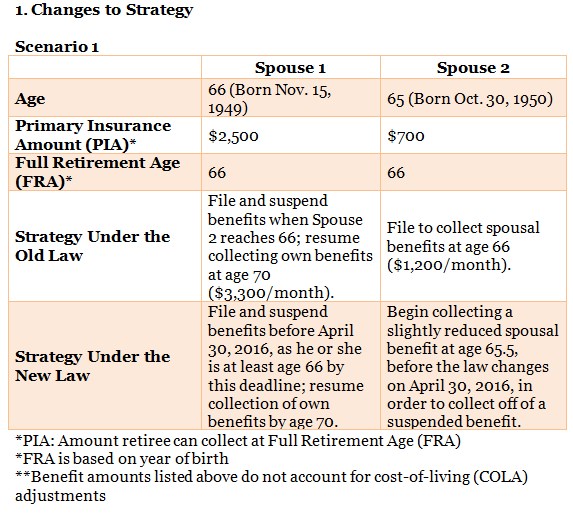

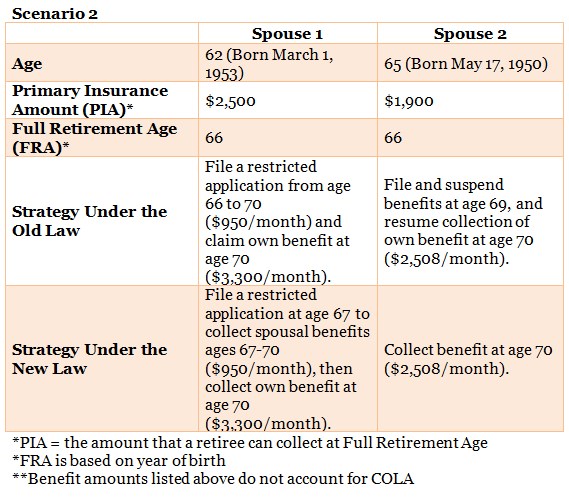

She offered these tables below to show two scenarios involving married couples — the group most impacted by the recent law change. They compare collection strategies under both the old and new Social Security laws. The scenarios below exemplify 1) Changes to strategy, and 2) The impact on cumulative benefits as a result of the new law.

In the above scenario, Lott said, it is important that the spouses take action before April 30, 2016. This allows the couple to implement a nearly identical strategy to their original plan.

“In this particular scenario, Spouse 2 is so close to his/her full retirement age that filing before the law changes will only result in a slight trim in benefits, so this strategy remains optimal,” she said.

Please note these charts are very case-specific. If you or your spouse will be age 66 by April 30 and you have not yet filed for Social Security benefits, you should speak with your a financial advisor to see if you need to take action before this important deadline.

Under the new law, Spouse 1 in the above scenario can no longer collect spousal benefits until Spouse 2 has begun receiving his or her own benefit. This delays spousal benefit by one year, but a similar strategy can still be implemented to optimize the couple’s overall draw, Lott said.

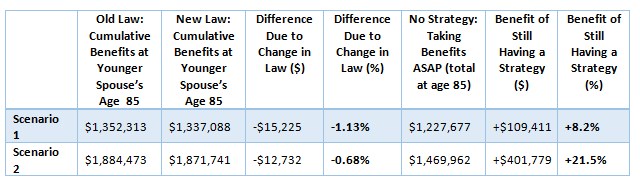

Now, exactly how much will you collect under the new law compared to the old law under these strategies?

*Cumulative benefits above include an annual COLA of 2.8%, as utilized in Social Security Trustees Annual Report projections.

Scenario 1 – The younger spouse starts benefits at age 66 under the old law, age 65.5 under the new law and for the older spouse at age 70 at under both the old and new law. With no strategy benefits start at age 65 for the younger spouse and age 66 for the older spouse.

Scenario 2 – The younger spouse starts benefits at age 66 under the old law, age 67 under the new law, and for the older spouse at age 70 under both the old and new law. With no strategy benefits start at age 62 for the younger spouse and age 65 for the older spouse.

As you can see from the table above, the new law decreases the couple’s total cumulative benefit in Scenario 1 by 1.13 percent, or $15,225 dollars, over their entire lifetimes, Lott said.

“Meanwhile, the benefit of using a proactive strategy under the new law — rather than just taking benefits as soon as possible — increases the couple’s yield by 8.2 percent for a total of $109,411 more received,” Lott said. “Likewise, due to law changes, the couple’s cumulative benefit in Scenario 2 is decreased by only 0.68 percent, or $12,732 dollars. The couple’s benefit grows by 21.5 percent, or $401,779, by using an alternative strategy under the new law.”

Lott said this tells us the recent law only decreases most people’s Social Security benefits by a relatively small percentage. More important, choosing a proper filing strategy can still make a significant financial difference.

Good luck with your personal calculations.

Email your questions to Ask@NJMoneyHelp.com.

This story was first posted in January 2016.

NJMoneyHelp.com presents certain general financial planning principles and advice, but should never be viewed as a substitute for obtaining advice from a personal professional advisor who understands your unique individual circumstances.