13 Nov Help! How do I pick the right mutual funds?

Photo: click/morguefile.comQ. I’m 50 and single. How can I decide what mutual funds I should be in?

— Need help

A. It’s a great question, but it’s not as simple as choosing mutual funds based on your age and marital status.

To give you an illustration, we turned to Bernie Kiely, a certified financial planner and certified public accountant with Kiely Capital Management in Morristown.

He assumed your long-term goal is to have a comfortable retirement. The Social Security Administration says the full retirement age for someone who is currently 50 year old is age 67, so that means you have 17 more years to save for retirement, Kiely said.

“Investing requires a plan, a destination: Where do you want to be in the future?” he said.

In order to find out your destination, you need to ask yourself some questions, Kiely said.

1. How much do you currently have saved?

2. How long will you live in retirement?

3. How much do need to spend in retirement?

4. How much can you save each year for the next 17 years?

5. What is your risk tolerance?

Your answers to those five questions all fit together like a mathematical formula, Kiely said.

“Your tolerance for risk plus your ability to add to your retirement savings are directly related to the investment return you must achieve going forward,” he said. “If you are unable to accept any investment risk, you will have to save more every year. If, on the other hand, you are not afraid of risk, the amount you must save will be less.”

Kiely said there a few investment rules of thumb he uses:

1. Be properly diversified (asset allocation)

2. Rebalance periodically (asset allocation)

3. Buy good stuff (low expense index funds)

4. Save regularly

5. Don’t try to time the market

6. Invest with your head, not with your emotions

7. Absolutely, positively don’t panic in market downturns

Kiely said the first decision you must make is how much you want in fixed income and how much in equities.

Equity type investments — stocks — will grow and help offset inflation. Fixed income investments — CDs, bonds, etc. — are safer, and they will allow you to sleep at night.

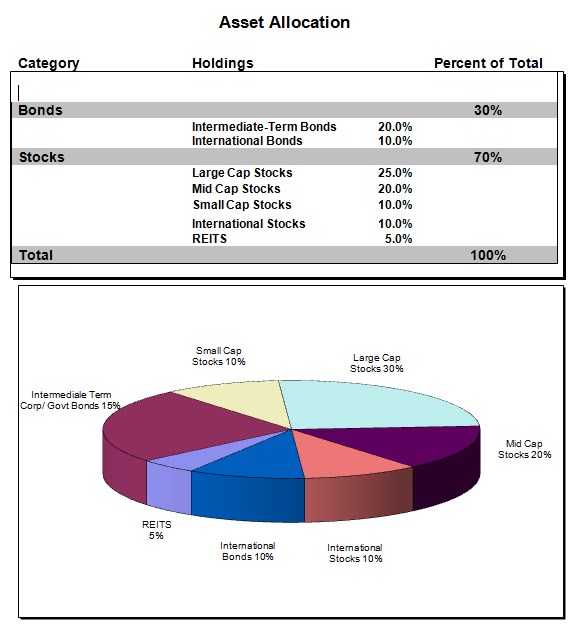

“I never recommend 100 percent in equities or 100 percent in fixed income,” he said. “For someone who is 50 and saving for retirement, I would probably recommend an allocation that was 70 percent equities and 30 percent fixed income.”

The next step is to take the equity portion and break it down to large-, mid- and small-cap, plus REITs and international stocks, Kiely said. The fixed income portion would be broken down into U.S. government, corporate and international bonds.

Source: Bernie Kiely, Kiely Capital Management

Kiely believes goal-oriented investing is what you need. He also doesn’t favor individual securities, but getting diversification from mutual funds.

“Individual stock selection with your life’s savings is gambling, not investing,” he said.

Kiely offers this 12-step plan:

1. Use no-load mutual funds. That means no front-end load, rear-end load or deferred-load.

2. In almost all cases, avoid 12b-1 fees. That’s money out of your pocket that will give you absolutely nothing in return. There are a very few cases where the overall expense ratio is so low that the 12b-1 fee can be ignored.

3. Select mutual funds that have at least three years of history. You can ignore this rule with index funds and exchange-traded Funds.

4. Select funds that have a manager with at least three or more years tenure.

5. Avoid funds with excessive turnover. There is ample proof that underperformance goes hand in hand with excessive trading.

6. Avoid style drift.

7. Match risk and return. A high-risk, low-return fund is not a good deal.

8. Avoid high capital gains exposure in taxable accounts.

9. When selecting between two funds, select the one with the lowest standard deviation.

10. When selecting between two funds, select the one with the highest Alpha.

11. Compare fund performance with its peer group not with the market as a whole.

12. Rebalance. Rebalance. Rebalance.

If you’re not comfortable taking all these steps on your own or if you don’t have time to do the research needed, consider hiring a financial planner to help.

Email your questions to .

This story was first posted in November 2015.

NJMoneyHelp.com presents certain general financial planning principles and advice, but should never be viewed as a substitute for obtaining advice from a personal professional advisor who understands your unique individual circumstances.