10 Dec What are my best options for Social Security?

Photo: lendingmemo.comQ. I’m 61 and my husband is 57. He will retire early next year, while I’m already retired and collecting a $1,450 monthly pension. Today he earns twice what I did when I was working. He will collect a pension worth the same amount when he retires, and he plans to work part-time. I plan to wait until my full retirement age to collect Social security, which will be $1,850 per month. We’re wondering if there are options between both of our Social Security benefits, such as him collecting a spousal benefit, so we can collect the most possible?

A. Congratulations on your retirements!

There are several scenarios to consider, but you’ll need to sit down with a rep at your local Social Security office to be sure of the benefits available to you.

Waiting until you reach full retirement age to collect benefits is a wise strategy because it prevents your benefit from being reduced by filing early, said Claudia Mott, a certified financial planner with Epona Financial Solutions in Basking Ridge.

“If you were to file at age 62, your benefit would be cut by 25 percent or more permanently,” Mott said. “Over a lifetime, that reduction can add up to a lot of lost income.”

While you aren’t able to claim your own Social Security benefit and a spousal benefit as well, there are a number of different filing strategies that you may wish to consider, she said. But, the most important part of that decision really depends on the cash flow you need to cover your living expenses,” she said.

For starters, your husband cannot collect a spousal benefit off of your earnings record at age 62 and then switch to his own benefit at his full retirement age, said Amanda Lott, a certified financial planner with RegentAtlantic Capital in Morristown.

“This is because your husband’s own benefit is likely higher than his spousal benefit off of your record.” she said. “His spousal benefit off of your record would be $925 (50% * $1850) and that’s if he started collecting at full retirement age.”

Lott said his own retirement benefit at full retirement age would probably be higher than that because you said he earned twice as much as you did and your own benefit is $1,850.

Until your husband reaches full retirement age, Lott said, he does not have the ability to choose which benefit he collects, but he simply gets the higher of the two. Therefore, if he starts collecting at age 62, he will be deemed to have started collecting his own benefit, she said.

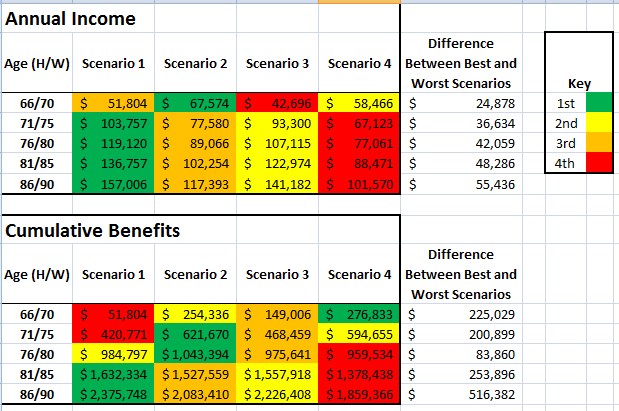

Lott created this chart — which includes cost of living increases — to show you many of the possible scenarios, all dependent on when you both choose to take benefits.

You can see from the summary chart that assuming you live long enough, Scenario 1 is optimal.

“However, you said that you don’t think you could financially wait this long to start collecting Social Security benefits,” Lott said. “Knowing that it would be a silly financial decision to go into credit card debt all in the name of delaying your Social Security benefits, Scenario 2 or Scenario 3 may be better options for you.”

Assuming that both are financially doable from a cash flow standpoint, if you live until your age 84 (age 80 for your husband), Scenario 3 would be optimal, she said. If you both die before then, Scenario 2 would be optimal.

“Given both of your current ages and assuming you are non-smokers, there is a 50 percent chance that you will live until age 88 and a 50 percent chance that your husband will live to age 85,” Lott said, based on mortality tables. “Barring any health concerns, the odds are in your favor for longevity.”

Email your questions to .

This story was first posted in December 2014.

NJMoneyHelp.com presents certain general financial planning principles and advice, but should never be viewed as a substitute for obtaining advice from a personal professional advisor who understands your unique individual circumstances.