18 Jun Do you have an exit strategy for your business or career?

by Peter McKenna, CFP®, MBA, Modera Wealth Management

Let’s face it, you aren’t as young as you think you are. While your body may let you know that the aging process is happening, your mind may play tricks on you. If you are like most of us, your self-image is a version of yourself ten to twenty years younger than reality. While this self-deception has benefits in some areas of your life, it can have significant drawbacks as it relates to business and career planning. This is especially true once you are in your 50’s or older.

Do you have an exit strategy for your business or career? Whether you are a corporate executive or a business owner, there will come a time when you want, or need, to transition to the next phase of life. Done in advance, this can be an optimistic process, it should define how YOU want to exit. As the plan develops, there will be reality checks and alternative paths to consider, but at this point it should be a framework of how you want the future to look. If not done in advance, it will be reactive and prone to unnecessary doubt and anxiety at an already stressful time.

A Preliminary Plan

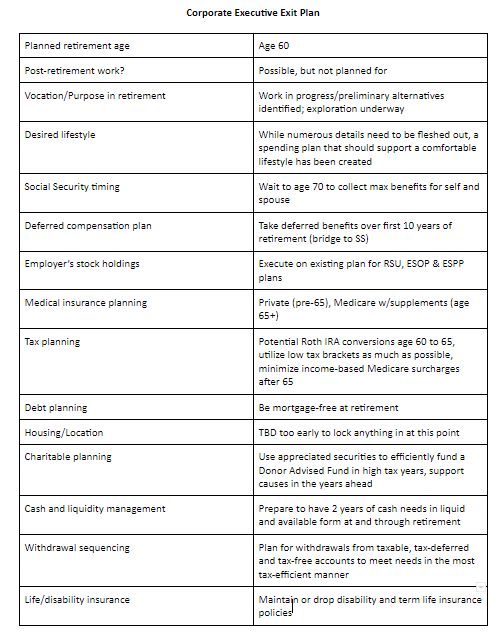

While the process should be entered with an “expect the best” approach, my tendency is to add some elements of “plan for the worst” as well. Using a corporate executive as an example, here is the type of exit plan I like to create with clients:

This example is for a corporate executive, but many of these elements are critical for business owners too. Business owners would have more planning related to the business, e.g., transitioning the business to successors, optimizing for sale and funding future lifestyle with the proceeds of the sale.

Ongoing Evaluation

The expression “The plan is nothing, the planning is everything” comes to mind here. While we create these detailed and complex plans, we know that the first change in assumptions, or reality, will make the original plan inaccurate. That doesn’t mean the plan isn’t serving its purpose. While those small changes mean the plan has to be adjusted, without the plan how are you going to evaluate your options when confronted with a big decision? As you approach the point of being ten years or less from your planned or likely exit, you need to have a framework in place to evaluate your options.

Here are some of the decisions a plan can help you with:

- Exploring post retirement purpose/vocation and what is possible for you

- What do you gain or give up by retiring sooner? Or Later?

- Evaluating early retirement offers in the context of your life

- How does a consulting arrangement impact lifestyle, taxes, etc.

- Sale of your business to family, employees, outside investors

- Real Estate transactions – e.g., second home, relocation, downsizing, commercial real estate (possibly including your business location)

- Financial and time capacity to support parents, children, siblings, and organizations

- Legacy planning and Charitable Giving

- Evaluating Social Security options

This list is not exhaustive as there are a number of considerations that will be more or less important to you. If you don’t yet have a plan, what is preventing you from creating one? If you don’t have time to plan now, when will you? Will that be early enough to give you time to create a plan before circumstances force you to make major life decisions?

To learn more about the ways Modera can help you as you consider your exit strategy, please contact us.

Peter McKenna, CFP®, MBA is a CERTIFIED FINANCIAL PLANNER® professional with Modera Wealth Management, LLC in Westwood, NJ. He may be reached at peterm@moderawealth.com or 201-768-4600.

Modera Wealth Management., LLC (“Modera”) is an SEC-registered investment advisor with places of business in Massachusetts, New Jersey, Pennsylvania, North Carolina, Georgia, and Florida. Modera may only transact business in those states in which it is registered or qualifies for an exemption or exclusion from registration requirements. SEC registration does not imply any level of skill or training. For information pertaining to our registration status, fees and services, please contact us or refer to the Investment Adviser Public Disclosure web site (www.adviserinfo.sec.gov) to obtain a copy of our disclosure statement set forth in Form ADV Part 2A. Please read the disclosure statement carefully before you invest or send money.

This article is limited to the dissemination of general information about Modera’s investment advisory and financial planning services that is not suitable for everyone. Nothing herein should be interpreted or construed as investment advice nor as legal, tax or accounting advice nor as personalized financial planning, tax planning or wealth management advice. For legal, tax and accounting-related matters, we recommend you seek the advice of a qualified attorney or accountant. This article is not a substitute for personalized investment or financial planning from Modera. There is no guarantee that the views and opinions expressed herein will come to pass, and the information herein

should not be considered a solicitation to engage in a particular investment or financial planning strategy. The statements and opinions expressed in this article are subject to change without notice based on changes in the law and other conditions.

Investing in the markets involves gains and losses and may not be suitable for all investors. Information herein is subject to change without notice and should not be considered a solicitation to buy or sell any security or to engage in a particular investment or financial planning strategy. Individual client asset allocations and investment strategies differ based on varying degrees of diversification and other factors. Diversification does not guarantee a profit or guarantee against a loss.

This is a sponsored section. The advisors have paid a fee to post their commentary here. Their sponsorship doesn’t influence any editorial decisions we make at NJMoneyHelp.com, or give them more or less exposure in our stories. Their posting does not constitute an endorsement by NJMoneyHelp.com.