13 Nov Required distributions and your Medicare premiums

Photo: pixabay.comQ. I retired this summer and just turned 70 ½ on Oct. 27, 2018. I have questions about Required Minimum Distributions so I can avoid paying more for Medicare Part B. Can I take part of my RMD in 2018 and part in 2019, and then my second RMD at the end of 2019?

— Senior

A. You raise two issues in your questions: Medicare Part B premiums and Required Minimum Distributions from qualified retirement accounts.

Let’s start with Medicare.

Medicare Part A covers the cost of a hospital bed, nursing care and the hospital food, said Bernie Kiely, a certified financial planner and certified public accountant with Kiely Capital Management in Morristown.

He said Medicare Part A is free although you paid into the system over your entire working life.

Medicare Part B covers doctors’ fees and outpatient care.

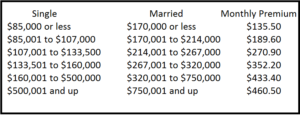

“Medicare Part B premiums are based on your modified adjusted gross income (MAGI) on your federal income tax return from two years ago,” he said. “So 2019 Medicare Part B premiums are based on your 2017 income tax return.”

If you file for an extension for your 2018 tax return, it won’t be due until by October 15, 2019, he said. That’s why they go back an additional tax year.

Here are the Medicare Part B premiums for 2019:

Now let’s take a look at your Required Minimum Distribution (RMD) from your qualified retirement plan.

You must take your first RMD by the year after the year you turn 70½, he said.

“You stated that you turned 70½ on October 27, 2018,” he said. “That means you can put off your first RMD until 2019.”

If you put it off, you will have to take both your age 70 RMD and your age 71 RMD in 2019.

“That may or may not be a good idea. You would have to run the numbers to see what would be best,” he said. “Most likely you would be better off taking your age 70 RMD this year and then one RMD each year after.”

Kiely said each year’s RMD stands by itself.

To determine the RMD, each year you would take the value of all your qualified retirement accounts as of the end of the prior year and divide by a factor. The factor is based on the attained age you reached in that calendar year.

For you, in 2018 you turned 70 and in 2019 you will turn 71.

So you calculate your RMD by dividing your Dec. 31, 2017 retirement account balance by 27.4 – from the IRS’ Uniform Lifetime Table, Table III – and in 2019 you would divide your Dec. 31, 2018 account balance by 26.5, Kiely said.

“Every year you must take the entire RMD by the end of that calendar year. If you take out too little, you pay a penalty,” he said. “If you take out too much you don’t get a credit in the subsequent year.”

The next year, you have to take out 100% of that year’s RMD.

There is one exception for the first year,” Kiely said.

“You can put off your first RMD until the year after the year you turn 70½,” he said. “o you want to take half of your 2018 RMD in 2018 and the other half before April 1, 2019, plus 100 percent of your age 71 RMD by the end of next year. I think that would work.”

But still, you need to run the numbers. If you want to make sure your income is below a certain level for Part B premiums, consider working with a financial professional who can help you do the math and not make a costly mistake.

Email your questions to .