04 Apr Where do inheritance tax monies go?

Photo: hotblack/morguefile.comQ. Where do inheritance tax monies go and how does it actually get there?

— Curious

A. Ah yes, the infamous New Jersey inheritance tax.

The tax is payable to the New Jersey Division of Taxation, and it’s added to the state’s coffers.

The tax return and payment is filed by the executor of the decedent’s estate, said Matthew Masterson, a certified financial planner with RegentAtlantic in Morristown.

He said New Jersey banks and financial institutions generally require a waiver to release the funds before they can be released to a beneficiary. The waiver is a written consent from the New Jersey Division of Taxation stating that assets can be released and is the process to ensure that payments are received.

Masterson said the inheritance tax is imposed based on the relationship of the person inheriting assets to the decedent.

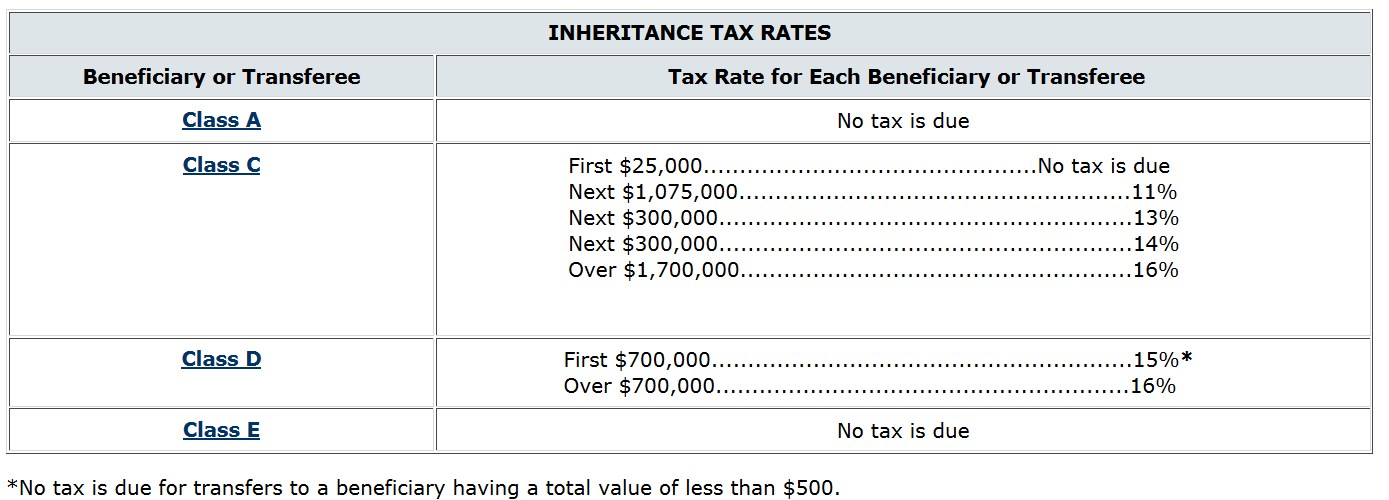

The beneficiaries of assets are broken down into four different classes: Class A beneficiaries are spouses and their decedents, and they’re exempt. Class C beneficiaries include brothers and sisters of the decedent, and others. Class D beneficiaries are a catch all, and include anyone not in any of the other classes. Finally, Class E beneficiaries include non-profit organizations which are exempt from the inheritance tax.

Below is a helpful chart from the State illustrating the tax rates imposed on each class.

Masterson said while New Jersey’s estate tax is scheduled to go away beginning in 2018, there are no such plans for the inheritance tax.

“Currently, the taxes are structured to offset each other so that both are not paid but with the estate tax being eliminated, many more estates will be subject to the inheritance tax,” he said.

Masterson said the tax can be quite burdensome for folks who wish to give assets to those outside their immediate family and can be difficult to plan around.

Email your questions to .

This post was first published on April 4, 2017.

NJMoneyHelp.com presents certain general financial planning principles and advice, but should never be viewed as a substitute for obtaining advice from a personal professional advisor who understands your unique individual circumstances.