21 Jul Snowbird balances risk with reward

We first met George in the summer of 2009, when he reached out to Get With The Plan, The Star-Ledger’s money makeover series that’s been reinvented by NJMoneyHelp.com.

The single man wanted recommendations on how to help his portfolio recover from the hit it took when the market collapsed in 2008.

At that time, it was suggested that his predominantly large-cap portfolio be diversified among different asset classes including small-cap, international and fixed income. The recommendation was also to reduce the cash position, which at the time was more than 50 percent of his investment assets.

Over the past seven years, George purchased a second home in Florida. His investment and retirement accounts have bounced back, and now, at age 61, George is looking to become semi-retired.

“For around the next 10 years I’d like to split my time with 5 1/2 months in New Jersey in the summer and 6 1/2 months in Florida in the winter,” he said.

George plans to continue working at least part-time in one or both of the locations, but he hopes it will be because he wants to rather than because he needs to.

“My goal is to have enough money that I can stop having to work as early as 62 or as late as 66 1/2,” he said. “And making sure I don’t outlive my money and can still live comfortably.”

We asked Claudia Mott, a certified financial planner with Epona Financial Solutions in Basking Ridge, to review George’s finances for NJMoneyHelp.com.

“The outlook for the future is brighter when George works part-time,” Mott said.

Let’s see how he can get there.

CASH FLOW

George currently works as an independent contractor earning about $68,000 a year, and he figures he will keep earning about half that amount until age 70.

Given his modest living expenses, he has been able to meet his needs between his earnings and the interest and dividends from his investment accounts, Mott said.

By lowering his annual income, he will need to address a cash flow shortfall.

“He would need assets of $1.079 million generating 3 percent income to fund the estimated cash flow shortfall,” Mott said. “With a portfolio of $1.2 million currently, he should be able to earn what he needs.”

Until George reaches full retirement age of 66 years and 4 months and begins to collect Social Security, Mott said, he will need to cover his cash flow shortfall from his assets.

He should start by tapping his money markets so his invested assets can continue to grow, Mott said.

“Although it may be tempting to file for Social Security immediately upon reaching age 62, this will result in a permanent 25 percent reduction in benefits for a lifetime,” she said. “With a large pool of resources to cover the cash flow shortfall, George should consider waiting until full retirement age to file.”

His monthly benefit at that time will be $26,856 per year. If he filed early, he would receive only $19,572 annually.

Waiting until age 70 would bring an even larger benefit of $34,788 a year.

“This is certainly an option he might entertain as it would reduce the amount he would need to draw from his investment accounts once he stops working,” Mott said. “If he has a history of family longevity and no significant health problems, this choice would result in additional lifetime benefits of $75,000 or more were he to live past age 92.”

Regardless of age or employment status, everyone should plan to have an emergency fund to cover unanticipated expenses, surprise repairs or unexpected purchases, Mott said.

“While there is no hard and fast rule for retirees, it is often considered prudent to keep 9 months to a year’s living expenses in a liquid savings account or CDs,” she said. “For George, this would mean preserving at least $60,000 in a savings account or ladder of CDs.”

As of now, his emergency fund is more than fully funded.

INFLATION

George says his risk tolerance is about average but also says he’s now more concerned with wealth preservation than improving growth by adding risk.

His current portfolio is comprised of 43 percent cash and equivalents, 15 percent fixed income and annuities, and the remainder in mutual funds, ETFs or individual stocks.

The high cash position would align with a far more conservative risk preference than average, Mott said.

“While George may wish to avoid any further market meltdowns like that of 2008 by maintaining a high cash position, he leaves himself at risk for the impact of inflation,” she said.

For example, a CD earning 1 percent interest in today’s rate environment is actually losing about 1.5 percent in real terms when compared to inflation, Mott said. This may not be a significant problem now, but if inflation increases, even by 1 percent, it will impact the portfolio’s ability to meet the higher level of expenses that will result, she said.

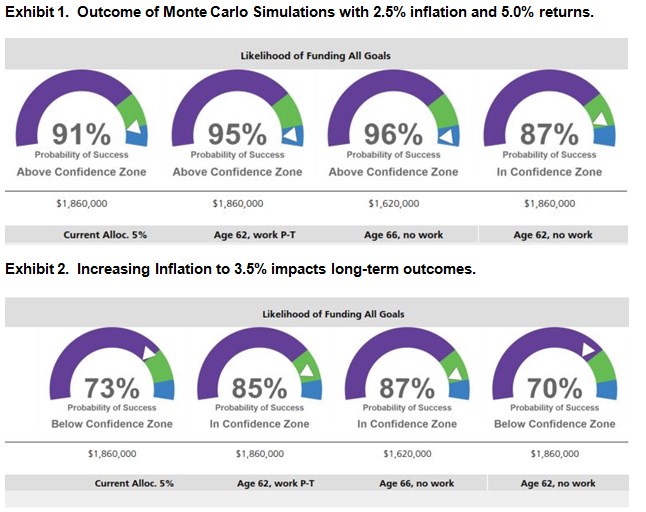

Mott ran Monte Carlo simulations, which look at 1,000 different scenarios of return patterns to see how a portfolio could weather different outcomes.

The simulations show a change in inflation from 2.5 percent a year to 3.5 percent a year would have a significant impact on George.

With the lower inflation rate, George’s current plan — assuming he retires at 62 and doesn’t work — shows he has a 91 percent chance of not running out of money by age 92. If all is the same but the inflation rate rises to 3.5 percent, George’s probability of success drops to 73 percent.

One of the factors contributing to the positive outcome for George is the low withdrawal rate from his portfolio in order to meet his living expenses, even when adjusted for inflation, Mott said.

“Generally it is suggested that retirees plan for a maximum 4 percent withdrawal rate in order for their portfolios to last through retirement,” Mott said. “In George’s plan, he is well below 4 percent throughout his 70s and early 80s.”

It’s important for George to consider future changes in his expenses.

Until George reaches age 65 and can apply for Medicare, he will need to continue to obtain health insurance directly from a company offering individual plans.

“The cost of these plans will increase as he gets older and those additional expenses need to be factored into his budget for the next few years as they will affect his cash flow needs,” she said. “Were his expenses to rise from the current $60,000 to $73,000, the probability of a successful retirement falls into the mid-70s.”

He should also consider what might happen if he needs long-term care.

Mott said if he’s interested in protecting his portfolio and the potential risk that a serious illness might play in greatly reducing its value, having a conversation about long-term care insurance may be worthwhile.

ASSET ALLOCATION

George’s current asset allocation has more than 40 percent of his assets in cash and CDs. While this appears to meet George’s needs throughout retirement at current inflation levels, he should consider whether he can further enhance his portfolio’s potential by including bonds and perhaps making some changes in his equity holdings, Mott said.

She said a well-designed bond ladder can create income over time and becomes a source of cash when the bond matures.

“The ladder is set up to meet increased long-term cash needs such as those that George will likely have later in life as a result of inflation outrunning the growth of Social Security benefits,” she said.

If this was built within his retirement account, Mott said, he would not incur taxes on the periodic income payments because of the account’s tax-deferred status. He could also use municipal bonds if he chooses to transition some of the CDs as they come due.

With 77 percent of the equity holdings in his retirement account considered large-cap U.S. stocks, the portfolio is lacking in exposure to international stocks, which Mott said could be fulfilled with a well-diversified mutual fund or exchange-traded fund.

Additionally, she said, George may want to review the individual stocks in the plan to be sure that they are meeting his expectations.

“In a quick review of the holdings I noted that nine of the positions have lost money on a three-year average basis and of those, five are also down over the past five years,” Mott said.

But overall, assuming a 5 percent long-term rate of return, Mott said George should make it, so he has some flexibility in terms of when he actually stops working.

“George’s portfolio should see him through to the end of a long and happy retirement as he splits his time between New Jersey and Florida,” she said.

Money makeovers offered by NJMoneyHelp.com should be treated as general advice about personal finance and money decisions. Before you make any changes to your personal financial plan, see a professional who can consider your entire financial situation. If you’d like a free money makeover, email Ask@NJMoneyHelp.com.Net Worth:

Assets:

- Checking: $25,600

- Money markets: $235,600

- CDs: $276,900

- IRAs: $641,000

- Brokerage Account: $230,700

- N.J. home: $375,000

- Florida home: $175,000

- Personal Property: $30,000

- Autos: $46,500

Total Assets: $2,036,300

Liabilities:

- none

Total Liabilities: $0

Total Net Worth: $2,036,300

Budget:

Annual Income:

- Earnings: $68,000

- Investment Income: $$23,800

Monthly Expenses:

- Income Taxes: $875

- N.J. housing: $736

- Florida housing: $315

- Utilities: $390

- Food: $200

- Education: $126

- Personal Care: $20

- Transportation: $368

- Medical: $897

- Entertainment: $69

- Vacations: $43

- Charity: $16

- Gifts: $10

- Misc.: $100