14 Jul Special report: Are we headed for a downturn?

The election of President Donald J. Trump has been good for investors.

From Election Day to this writing, the Dow Jones Industrials Average is up more than 18 percent and the Nasdaq Composite is up more than 21 percent.

Whatever you think of the president personally, you should be cheering for your portfolio.

But — and yes, there’s always a but — how long will it last? Could we be heading for a downfall?

You know we don’t go for “scare” reporting, but with so many big changes happening to our country, we’d be remiss if we didn’t ask the question — especially as the stock market keeps heading higher.

In this NJMoneyHelp.com Special Report, we take a closer look at why stocks have reacted so positively to our often-controversial president. More importantly, we tackle what we as investors — with our retirement wishes, mortgages and college payment obligations — should do going forward.

Sit back, grab a cup of coffee, and brace yourself for a big dose of reality.

WHERE WE ARE, HOW WE GOT HERE

Pretty much the whole world expected Hillary Clinton to win the election, so the markets, like most others, had a big surprise.

The realization that pundits were wrong caused an overnight selloff — Dow futures were down more than 900 points overnight — but the markets came back with a bang. The Dow closed up more than 250 points.

It hasn’t been a straight line since then, but investors took a bet on the new administration. So far, they’re winning.

Consumer confidence and surveys that predict future hiring for small businesses both took leaps after the election, said Stephen Craffen of Stonegate Wealth Management in Oakland.

Others believe the economy will grow faster under an administration that has promised to reduce taxes, regulations and government interference in the economy, he said.

“Most economists will admit that the actions of the prior administration have led to a relatively weak recovery after the financial crisis of 2008,” Craffen said. “Those increases in confidence are leading to the stock market’s excellent performance over the last eight months.”

But now, as the Trump administration settles into its job — and its relationship with Congress — some of those hopes are slowing.

Tax and regulatory reform hasn’t happened as quickly as some may have liked. Others question how much work will actually get done in Washington as factions of the Republican party haven’t come to an agreement on much of anything.

The portions of the market with the most to gain from tax and regulatory reforms have actually lagged, said Andy Kapyrin, director of research at RegentAtlantic in Morristown.

He said smaller U.S. companies that tend to do more business on our shores have underperformed their larger peers because they had the most to gain from the potential reform, which now seems further out.

Improvements in earnings have been real, though, Kapyrin said.

“For the first time since 2011, large American companies are posting double digit gains in earnings per share,” he said. “I believe this is the biggest driver in share price gains and the biggest reason they’ve continued to do well in spite of politics getting more complicated.”

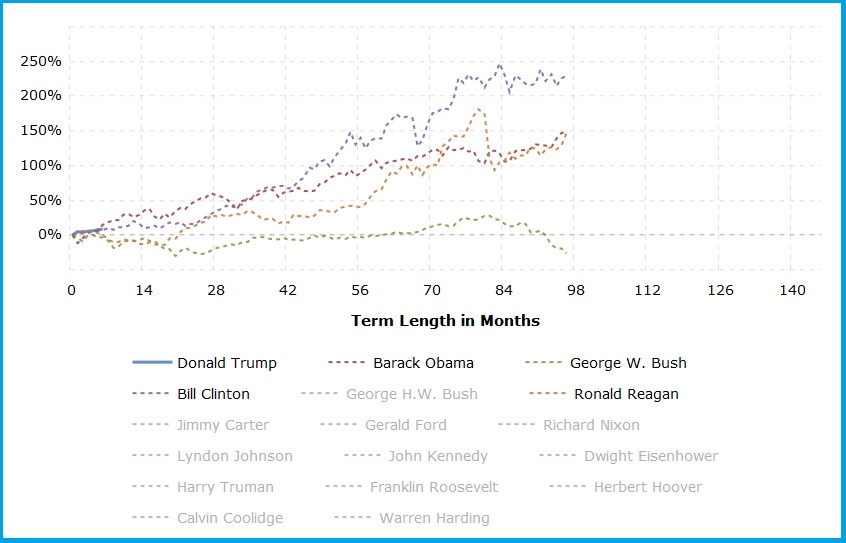

Diahann Lassus, a certified financial planner and certified public accountant with Lassus Wherley in New Providence, said she isn’t sure the higher market is Trump-specific because stock performance tends to be good in election years in general.

She pointed to the chart below, which shows a positive trend for stock performance during the first six months for most recent presidents.

The chart shows, in descending order, the Dow went up 14.6 percent during President Barack Obama’s first six months, 8 percent during President Donald Trump’s first six months, 6.9 percent for President Bill Clinton’s first six months and it fell 3.3 percent for President George W. Bush’s first six months.

Lassus said Trump inherited an economy that was growing consistently but at a slower rate than many would like.

“We are in the ninth year of economic expansion, the second longest on record. We also had a very low unemployment rate paired with low interest rates,” she said. “The reality is that the market, or rather, investors, are usually looking at the economy and earnings first and other things second.”

She said investors certainly like the idea of lower tax rates and investment in infrastructure.

“If it looks like Washington is moving forward with tax reform and they figure out a way to support more infrastructure projects, that may help keep the markets in a positive place for a while,” Lassus said.

But what if those big legislative efforts don’t happen?

THE FUTURE OF TAX REFORM

If investors have been counting on pro-business legislation in general — and tax reform specifically — there could be big disappointment if it doesn’t happen.

After seven years of promises to repeal the Affordable Care Act — Obamacare — delays and Republican in-fighting have put a damper on Congress’ ability to move forward with any significant legislation.

Lassus said she’s not sure there really is an expectation of tax reform now.

“If the House is able to come up with a reasonable approach for broad-based tax reform that makes sense for more than just the high net worth individuals, it could actually drive a more positive reaction in the financial markets,” Lassus said. “However, I would not hold my breath waiting for a solid compromise bill to come out of the House or the Senate at this point.”

The promise of tax cuts is a key element that’s contributed to an increase in stock prices in the recent past, said Charles Pawlik, a certified financial planner and chartered financial analyst with Beacon Trust in Morristown.

He said uncertainty over tax cuts could drive short-term volatility in the markets, but he said it’s important not to make any large shifts in your portfolio based on speculation surrounding tax or other policy initiatives.

Pawlik said we probably won’t see any meaningful progress until 2018.

If nothing happens immediately, it won’t be a huge deal, Kapyrin said. But if nothing happens by this time next year, in July 2018, it would be a bigger problem, he said.

“The mid-term elections could change the balance of power adversely for Republicans and make meaningful tax reform, or even a tax cut, harder to enact,” he said.

Craffen said if a large tax cut has already been baked into current market valuations, not getting legislation passed would be a major concern.

He said the U.S. has one of the highest corporate tax rates in the world at 35 percent, and there’s been talk the rate could be lowered to 15 or 20 percent. There’s also a belief that corporations may be able to efficiently repatriate money they have held overseas if the lower tax rates come to pass.

“Delaying tax legislation could lead to a market correction, especially if corporate profits do not grow or if the gross domestic product (GDP) remains stuck at a 1 to 2 percent annual growth rate,” he said.

WHAT ABOUT RUSSIA?

Given that the markets hate uncertainty, we wanted to know why investors haven’t gone running for the hills with all the questions about Russia.

History shows speculation can give investor confidence a huge hit.

Not this time.

The Russia investigation, shake-ups of high profile government positions and questions about the stability of the administration have added to political uncertainty, Pawlik said.

That leads to questions about Trump’s ability to implement the pro-growth agenda that Wall Street is counting on, he said.

“Markets have continued to rise in the face of this, likely due in part to the idea that if President Trump were to actually get impeached at some point, Vice President Pence is likely to continue to work towards the same pro-growth policies such as tax cuts and deregulation,” Pawlik said.

He said solid corporate earnings expectations, generally good economic data, slow but steady GDP growth and investor confidence all continue to contribute to gains in the market.

Craffen said the Russia investigation has not been of interest to most people, calling it a “media infatuation.”

“Few other than extreme partisans believed it would lead to any revelations that might cause some major change in leadership in this country or the policies of the administration — which are probably responsible for the market’s performance over the last eight months,” he said. “The relative unimportance of this is reflected in the lack of volatility in the markets.”

Lassus said investors and the market in general are taking a wait-and-see approach.

She said she expects volatility to pick up over the summer and into the fall depending on the headlines and, of course, earnings for the next quarter.

“The financial markets and investors typically dislike uncertainty but it is difficult to assess what impact any news concerning the ongoing investigations will have on the markets at this point,” she said. “Many investors seem to be building this in as background noise versus the front-and-center issue some believe it needs to be.”

Kapyrin said it’s important to separate reality from political tendencies of hyperbole.

He called the Trump administration’s ties to Russia “worrying,” saying an investigation could find a smoking gun.

“That would be a bad, destabilizing development and would derail most hopes for political developments from Washington, D.C.” he said. “In the absence of concrete evidence, though, it becomes just another scandal that takes up air time on the news but means little at the end of the day.”

For now, he said, Trump’s Russia ties make for great headlines, but little damning evidence has surfaced.

GETTING TECHNICAL: ARE VALUATIONS TOO HIGH?

With the U.S. stock markets at or near their highs, investors need to understand whether prices and valuations are inflated or if they’re real.

Valuations give investors an indication of how “expensive” or how “cheap” markets may be relative to historical averages.

Pawlik said when valuations are elevated, it could — but won’t always — lead to a downturn.

He said today, the market is “relatively expensive” based on some commonly followed data.

As of June 30, he said, the forward one-year price-to-earnings ratio, or P/E ratio, for the S&P 500 was 17.5. That compares to the 25-year average of 16.0.

When you look at shorter-term averages, P/E ratios look more elevated, he said. For example, the five-year average forward P/E is 15.3, and the 10-year average is 14.0.

Kapyrin agrees that valuations are above average right now.

“At this valuation, stock returns are likely to be lower than average going forward,” he said. “I believe a number of factors have driven valuations higher – optimism about politics, improving economic conditions and the feeling that the U.S. is a safe haven from volatility abroad.”

Looking overseas, this could mean an opportunity, he said.

If the U.S. has above average valuations, the rest of the world is closer to its norms or downright cheap, Kapyrin said.

“Investors should look at their portfolios and see if they have enough invested abroad, especially in the emerging markets which are experiencing a resurgence this year on the back of better economic news,” he said. “Their valuations continue to be well below ours.”

Craffen agrees P/E ratios are high but says they’re not necessarily “excessively high.”

He said it’s important to remember there are two pieces to a P/E ratio: current stock prices and current corporate earnings.

The ratio can drop into a more conservative value if stock prices decline or corporate profits increase, Craffen said.

“If the ratio drops because of an increase in corporate earnings, that would be good for investors since while stock prices may not increase like they have, the current valuation for the market might be `real’ and might stabilize without stock prices declining.” he said. “Therefore, there may not be a severe `correction.’”

Higher valuations don’t necessarily point to an impending downturn in stock prices, Pawlik said, noting valuations can remain elevated for an extended period of time.

He said there’s a very low correlation between valuations and the subsequent returns of the stock market over the short-term, “boiling down to the fact that valuations don’t tend to have all that much explanatory power relative to what stock market returns may be over the next 12 months.”

Valuations tend to provide a better indication of where stock prices may go over the longer-term than they do in the short-term, Pawlik said.

Lassus said it’s also important to consider valuations for fixed income, which often have a healthy allocation in investor portfolios.

She said U.S. investment-grade fixed income is a market with stretched valuations.

“Fixed income has been in a bull market for more than three decades, resulting in rising bond prices and falling yields,” Lassus said. “We have experienced several false starts, but when interest rates rise, investors may encounter falling bond prices in their portfolios.”

LOOKING AHEAD

The advisors we spoke to are long-term investors who believe a diverse portfolio, over the long term, will help you reach your goals and protect you from volatility.

But if you’re nervous that the stock market can’t continue its gains, or won’t for long, what’s the average investor to do?

Our advisors agree you shouldn’t try to time the market, but instead, have an asset allocation plan that you stick to — with tweaks — for as long as it suits your needs and risk tolerance.

Lassus said her focus is always on investing in a broad-based, globally diversified portfolio and rebalancing periodically. That means you try to buy low and sell high to bring your portfolio in line with your strategic objectives. For example, she said, if your target for U.S. large caps is 25 percent and your large-caps have increased to 30 percent, it is time to take profits.

She said she doesn’t make bets on sectors or individual stocks

“We think right now is a really good time to make sure you have a true diversified portfolio, meaning not just a lot of mutual funds but making sure they are actually investing in different types of investments like U.S. large cap stocks, U.S. small cap stocks and other asset classes such as international large cap stocks and even emerging market funds,” Lassus said.

Pawlik said with the substantial run-up we’ve seen and being in the eighth year of a bull market, a downturn in the markets would not be unexpected.

But, of course, we never know exactly when that will be.

He said it’s important to remain focused on the long term and to invest in a diversified portfolio of assets that includes both U.S. and international equity and fixed income investments, as well as alternatives such as hedged strategies/risk-controlled investments that can help to mitigate volatility in a down market.

“Crafting and managing a well-balanced portfolio on an ongoing basis can position investors for growth when markets perform well, as well as provide downside protection when an eventual downturn in the markets occurs,” Pawlik said.

He also points out that positioning yourself too defensively based on an attempt to time the market can lead to missed opportunities. And then, you’re stuck with the significant challenge of deciding when to return to a more aggressive allocation.

Craffen said he’s not big on predictions, noting it almost always makes more sense to be broadly diversified both within an asset class like large domestic stocks, and by asset class.

“If you do want to try to choose sectors of the economy, consider owning a broad-based index fund for most of the money you devote to large stocks and then perhaps buy an exchange-traded fund that is focused on a sector of the market, for example energy with a much smaller amount,” he said. “That way you do not dramatically underperform the market if your `bet’ on a sector is not fruitful.”

The advisors have cautious optimism, but they also see that there could be some large potholes for investors in the next year or so.

You should rebalance your portfolio — be diverse if you aren’t already — and take some profits, they say. Put yourself in the right place so you won’t react emotionally in a downturn. Be sure you have enough cash on hand for emergencies.

And if the bad headlines come in, don’t panic.

We’ll be here to help.

If you want a second opinion on your investments, consider a free money makeover. Just send us an email at .

This post was first published in July 2017.

NJMoneyHelp.com presents certain general financial planning principles and advice, but should never be viewed as a substitute for obtaining advice from a personal professional advisor who understands your unique individual circumstances.