03 Feb Special report: Trump’s exec orders, your wallet

Investors might be excited about prospects for a higher stock market under President Donald Trump’s pro-business policies, but they should worry about steps the president took Friday to eliminate some rules that protect investors and consumers.

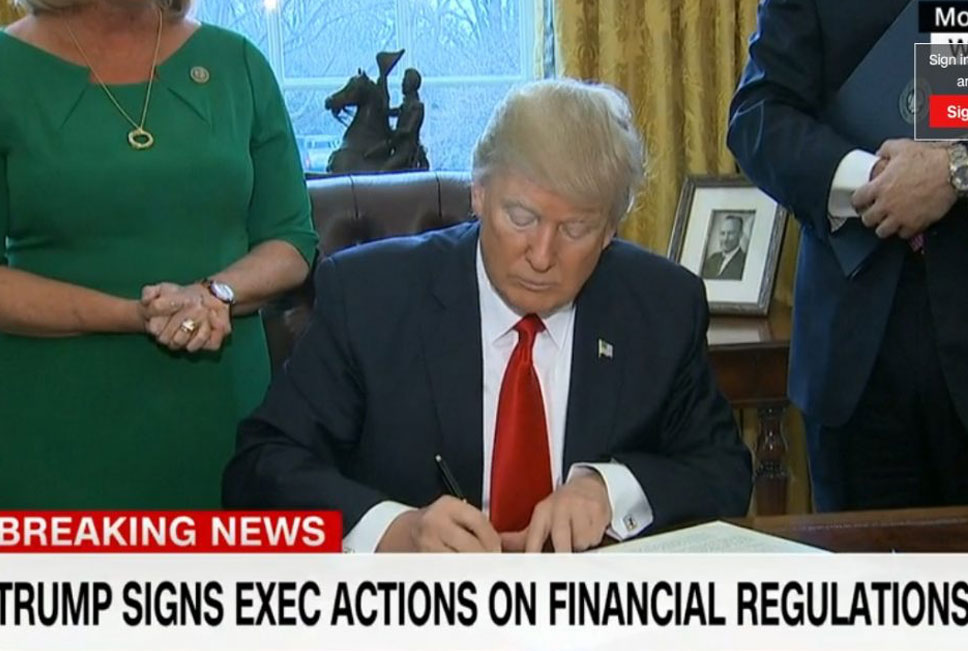

The moves, in the signing of two executive orders, are a prelude to softening financial regulations and removing consumer protections.

In the first executive order, Trump asks for a re-evaluation of regulations enacted after the economic crisis of 2008 by instructing federal regulatory agencies to give suggestions for reform.

That by itself may not seem like a big deal, but what it really means is that Trump is eyeing changes to the Dodd-Frank Wall Street reform law, which Trump has called a “disaster.”

The complex law has many parts, but it’s aimed at making sure banks can’t engage in the kind of abusive lending and mortgage practices that led to the recession. For example, it required banks to take annual “stress tests” to prove they could handle economic trouble.

Those requirements could be on the way out.

The second executive order, Trump basically squashes the newly expanded Department of Labor definition of “investment advice fiduciary,” which was set to be in effect in April.

Under the rule, all financial professionals who provide retirement advice or work on retirement plans would be considered “fiduciaries.” That means they’re legally and ethically bound to put the interests of their clients first.

This was important because while many advisors already work as fiduciaries, many others do not, and that makes it hard for an investor to decide whether the advisor is looking out for the investor’s best interests or looking for a higher commission when selling products and advice.

The moves are “strongly opposed” by the Financial Planning Coalition – a group made up of the Certified Financial Planner Board of Standards, (CFP Board), the Financial Planning Association (FPA) and the National Association of Personal Financial Advisors (NAPFA).

“With just two months to go before its implementation date, the president has effectively given the green light to maintain the status quo of conflicted financial advice,” the group said in a statement.

It said the president “is directing the Department of Labor to produce an outcome that will likely lead to either a complete gutting of this thoroughly vetted consumer protection or lead to its outright demise. Either one is a bad outcome for American retirement savers.”

Nicholas Scheibner, a certified financial planner with Baron Financial Group in Fair Lawn, echoed the sentiment.

“Although it only applies to retirement accounts, it is the first step in keeping all financial advisors legally bound to their clients’ best interests,” he said.

Undoing the fiduciary standard puts investors and consumers at risk, said Diahann Lassus, a certified financial planner and certified public accountant with Lassus Wherley in New Providence.

She said “fiduciary” is a much higher standard than the “suitability” standard brokers have typically operated under.

“‘Suitability’ only requires that the recommendation be appropriate to the client’s objectives rather than being in the client’s best interest,” Lassus said. “This is something that is needed today when individuals are struggling to save enough to retire with a 401(k) and IRAs because pension plans are quickly disappearing.”

She said with future retirees more responsible for their financial futures, “it becomes critical that advice is available that is designed to put the individual client’s interest first.”

On Dodd-Frank, Lassus said the act was the most comprehensive financial regulatory reform since the Depression.

She said consumers should be concerned about the future of the Consumer Financial Protection Bureau (CFPB), which was established to provide oversight of consumer financial markets such as student loans and credit cards.

Some have wondered if the new administration will try to dismantle the agency, which has, since 2011, recouped $11.7 billion for consumers and fined banks and other institutions $440 million in civil penalties.

Lassus warns investors that the lack of predictability of the current administration’s actions present a risk.

“On a day-to-day basis we and the world are constantly surprised with what comes out of the White House,” she said. “This leads to headline risk in the markets that can create significant volatility and lead to high investor fear. This fear can lead to even more volatility.”

She said most investors should review the emergency reserve they have set aside to verify it is adequate for their needs. Plus, they should look at their overall portfolio to make sure it’s in line with their objectives for the long term, and they should rebalance to take profits along the way.

“Don’t get more aggressive to take advantage of what some see as an even longer term U.S. stock market rally because there is no guarantee it will last,” she said. “Stick with that broadly diversified portfolio to ride out what could be a very bumpy market.”