03 Dec Self-employed retirement savings tips

Photo: DodgertonSkillhause/morguefile.comQ. I have an individual 401(k). What’s the best way to make contributions — as the employer or as the employee? Which is more beneficial for my taxes? I earn about $100,000 a year from my business.

— Hard worker

A. An individual 401(k) goes by several different names.

It’s also called a Self-Employed 401(k), a Solo 401(k), a Solo-k, a Uni-K or a One Participant K.

Whatever you call it, it’s simply a qualified retirement plan that was designed specifically for employers with no full-time employees other than the business owner or owners and their spouses, said Bernie Kiely, a certified financial planner and certified public accountant with Kiely Capital Management in Morristown.

Kiely said these plans have the same rules and requirements as any other 401(k) plan, but exactly how they work in practice depends on the kind of business you have: a limited liability company (LLC) or an S-Corporation.

For an LLC, the business owner wears two hats in a 401(k) plan — employee and employer — and contributions can be made to the plan in both capacities, Kiely said.

As an employee, the individual can make elective deferrals up to 100 percent of compensation — “earned income” in the case of a self-employed individual — up to the annual contribution limit. That’s $18,000 in 2015 and 2016, or $24,000 in 2015 and 2016 if age 50 or over, Kiely said.

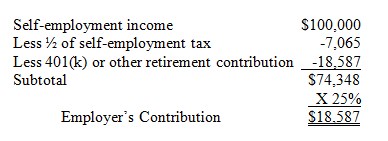

Then as the employer, non-elective contributions can be made up to 25 percent of compensation. Determining this amount is a little more complicated.

“When you calculate your compensation, you must reduce your net earnings from self-employment by the deductible portion of your self-employment tax, and the amount of your retirement plan contribution,” he said.

Kiely offered this example based on your $100,000 earnings.

The total you can contribute in 2015 is the sum of $18,000 (elective deferral) plus $18,587 (employer contribution) for a total of $36,587, Kiely said.

This amount should go on line #28 “Self-Employed SEP, Simple, and qualified plans, he said.

“As you can see if you are a Sole Proprietor, Partner or One Person LLC, your retirement plan contributions do not reduce your income for self-employment tax proposes,” he said.

And because there is only one line on the 1040 for the contribution, it does not matter which contribution you make, or which combination, Kiely said.

“They are basically one and the same, so one is no better or worse than the other,” he said. “They all go into the same retirement account and are not otherwise identified as to origin.”

If you instead are a working shareholder of an S-Corporation, you are an employee for purposes of pension plan contributions.

“As an employee, the Maximum Elective Deferral into a 401(k) plan is the same $18,000/$24,000,” Kiely said. “Your S-Corporation must set up a 401(k) Plan and make contribution through your payroll system.”

Your employer can then make the appropriate employer match contributions, he said.

The maximum contribution is based on what your S-Corporation pays you on a W-2. If, like many short sighted people, you “pay” yourself little or nothing in order to save payroll taxes, you can’t contribute to a pension plan, Kiely said.

“Pension and 401(k) contributions are based on your compensation or `earned income,'” he said. “Profits from S-Corporations is by statute “unearned income.”

Email your questions to .

This story was first posted in December 2015.

NJMoneyHelp.com presents certain general financial planning principles and advice, but should never be viewed as a substitute for obtaining advice from a personal professional advisor who understands your unique individual circumstances.