05 Jan Flipping the Switch: Generating a paycheck from your portfolio

by Brian Kazanchy, CFP, RegentAtlantic Capital

Dollar #1: “Hey, how did you get here?”

Dollar #2: “I was part of some Apple stock shares sold at a nice profit. How about you?”

Dollar #1: “That’s exciting! I was generated by a dividend on Chevron stock shares. Did you know the $100 bill next to you came from an interest payment on a New York muni bond?”

Dollar #3: “Nice to meet you. Looks we are all taking a trip to the restaurant cash register at the end of this expensive meal!”

The dialogue above is just a little humorous fiction, of course. However, the point is that once the after-tax proceeds of your investments are converted to cash, their buying power is identical. Some came from capital gains, others came from dividends or interest—and you really need access to all three of them to produce a comfortable portfolio for spending.

If you have ended your income-producing years or need to supplement your earnings with withdrawals from your portfolio, your general goal is to look to maximize all of those investment gains (while taking a risk level commensurate with your individual risk tolerance) to fund your lifestyle needs.

If those investment gains are maximized, the principal value of your portfolio may be left more intact and/or continue to grow. If that’s the case, then why has “generating income from your portfolio” become the popular phrase, rather than “maximizing investment gains” or “generating total returns?”

Perhaps it’s this: After decades of living off the income from paychecks, marketing professionals (and many financial advisors!) have been tempted to try to neatly replace the word “income” with “income”—even though we are talking about two very different meanings of the same word.

Benefits of Total-Return Investing

Total-return investing is a strategy that focuses on maximizing the combination of interest and dividend payments in a portfolio, along with capital appreciation. The primary components of portfolio income—interest and dividends—remain prominent in this strategy. However, they are also complemented by prudent risks intended to help achieve capital appreciation.

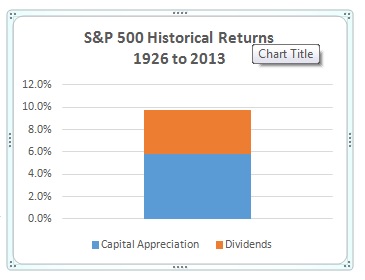

The chart (right) shows the important role capital appreciation has played in stock returns throughout history. Almost 60% of stock returns are generated through growth in the value of share prices, while the remaining roughly 40% has been generated by dividends.

The chart (right) shows the important role capital appreciation has played in stock returns throughout history. Almost 60% of stock returns are generated through growth in the value of share prices, while the remaining roughly 40% has been generated by dividends.

An investment strategy that can derive return from all sources—not just interest and dividends—can be better equipped to deliver returns over time, particularly in an environment where interest rates and/or dividend yields are low.

Dangers of Income-Focused Investing

Relying primarily on the income your portfolio generates rather than total returns can increase your risk and make everyday living more difficult.

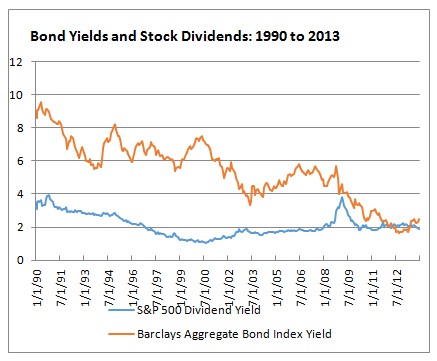

For example, yields in both bonds and stocks fluctuate over time. Since 1990, bond yields on the aggregate bond index have ranged from a high of 9.6% to a low of 1.6%. Stock dividend yields have been comparably more stable, but still ranged from 3.9% to 1.1%. (Source: Bloomberg)

As you can imagine, running a budget based on yields that fluctuate this dramatically could force you, as an individual investor, to make drastic lifestyle changes over time. Some years, your portfolio would generate generous amounts of income, while other years, it might not create enough income to cover a comfortable amount of your living expenses.

As you can imagine, running a budget based on yields that fluctuate this dramatically could force you, as an individual investor, to make drastic lifestyle changes over time. Some years, your portfolio would generate generous amounts of income, while other years, it might not create enough income to cover a comfortable amount of your living expenses.

Another common drawback of yield-based approaches is investors’ tendencies to increase their portfolio risk—in order to make more money—when income yields are low. The bond and stock chart illustrates how volatile income yields can be.

A fixed-income investor may seek to increase the maturity length or credit risk of bonds purchased in a low interest rate environment in order to increase potential yield. Similarly, a stock investor may seek to increase dividend yields by focusing more exclusively on sectors that pay higher yields, while excluding lower-yielding-sector stocks.

Both of these portfolio shifts can increase your investment risk dramatically. If you make these kinds of moves prior to a rising interest rate or recessionary period, your portfolio may suffer significantly higher losses than the overall bond and stock markets.

At the end of the day, the lesson is that a solely income-focused investing approach doesn’t do justice to the most fundamental question about an investment: Does this asset have a return potential that is commensurate with the risk I am taking by buying it? In many cases, the answer is no. On the other hand, adopting a total-return approach to investing can capture the best of both worlds—income plus appreciation—that you can use to more comfortably fund your lifestyle needs throughout retirement.

Brian Kazanchy is a certified financial planner with RegentAtlantic Capital in Morristown. He may be reached at or (973) 425-8420 x235.

This story was first posted in January 2015.

This is a sponsored section. The advisors have paid a fee to post their commentary here. Their sponsorship doesn’t influence any editorial decisions we make at NJMoneyHelp.com, or give them more or less exposure in our stories. Their posting does not constitute an endorsement by NJMoneyHelp.com.